Value-added tax

Value-added tax (VAT) is a consumption tax on the exchange of goods and services. Companies are obliged to add VAT to their prices and to invoice their customers accordingly.

Value-added tax within Germany

VAT is a consumption tax that is ultimately borne by the final consumer of a product or service. It is charged as a percentage of the price.

- 19 % is the normal rate in Germany at present.

- A reduced rate of 7% applies to certain consumer goods and everyday services (i. e. food, newspapers, local public transport, and hotel stays).

- Completely VAT exempt are some services like bank and health services or community work.

Companies must add the applicable VAT tax rate to value their prices

-

On purchasing goods or making use of services, companies regularly have to pay value-added tax themselves

-

The taxes collected and paid can be balanced out via input VAT deduction (Vorsteuerabzug).

-

Companies submit periodic VAT reports online to the tax authorities (Umsatzsteuer-Voranmeldung) on a monthly or quarterly basis using Germany’s ELSTER online tax office system. The frequency depends on the company’s level of turnover.

-

In addition, an annual VAT return (Umsatzsteuer-Jahreserklärung) must be submitted.

Business-to-business transactions

In specific business-to-business transactions, the business customer has to transfer the VAT to the tax authority – the so-called reverse charge procedure. This is applicable, for instance, to certain types of construction work carried out by subcontractors.

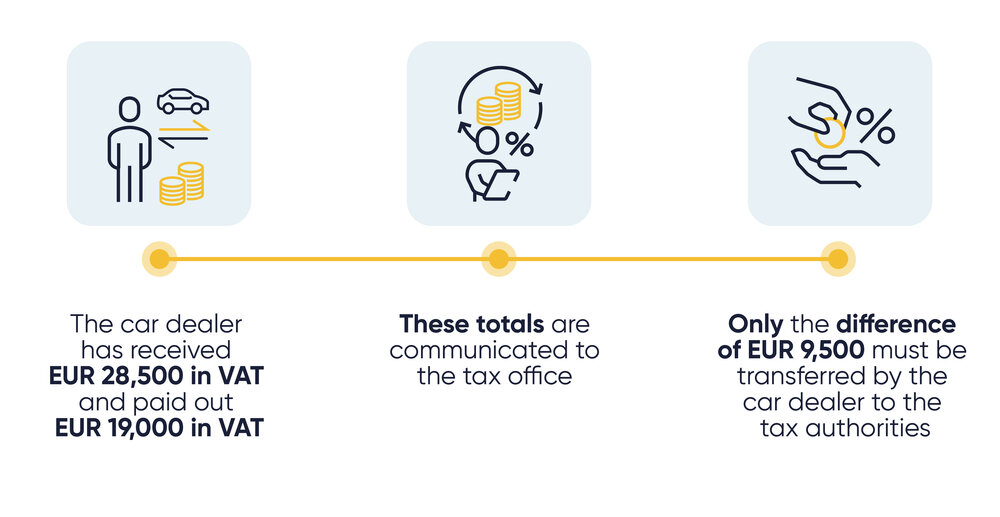

Example: how input vat is balanced

A car dealer has sold ten vehicles in one month, each at a gross price of EUR 17,850 (net cost EUR 15,000). For each sale, the dealer receives EUR 2,850 in VAT from the customer. At the end of the month, the dealer therefore owes the tax authorities EUR 28,500.

However, in the same period, the car dealer also bought ten cars from the car manufacturer. The net cost of each car was EUR 10,000. The car manufacturer added 19 percent VAT to this amount. The dealer therefore transferred EUR 119,000 (including EUR 19,000 in VAT) to the manufacturer.

Thus, the car dealer has received EUR 28,500 in VAT and paid out EUR 19,000 in VAT. These totals are communicated to the tax office (Finanzamt), and only the difference of EUR 9,500 must be transferred by the car dealer to the tax authorities.